![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

Since the start of January, the section steel market has been on a downward spiral, with prices continuously dropping and showing no sign of recovery. Many traders are now questioning whether this slump will eventually reverse or if it's just the beginning of a longer decline. The market is in a state of uncertainty, and the outlook remains bleak for many players in the steel industry.

The raw material billet market has also struggled to find stability after a prolonged period of weakness. Steel billet prices began to fall in mid-December, and although there was hope for a rebound in January, the market continued to disappoint. From 3,040 yuan per ton on December 30 to 2,820 yuan today, that’s a total drop of 220 yuan. In January alone, the decline reached 160 yuan, indicating a sharper fall than expected. Compared to 3,280 yuan per ton in the same period last year, the current situation looks even more challenging. This sharp drop has raised concerns among market participants, especially as inventory levels remain high.

As of January 23, the mainstream stockpiles of Tangshan billets reached 666,000 tons, with 187,000 tons added in January. This is significantly lower than the 431-104 million tons recorded in January 2013, which saw 610,000 tons added. Additionally, the operating rate of rolling lines in billet mills has dropped to around 20-30%, hitting a low point. These figures suggest that while supply is under control, demand is weak, leading to further price pressure.

One key reason behind the weak performance is the reduced purchasing behavior from downstream users. Many mills have cut their billet purchase volume from about 20 days to just 10 days, opting for a "just-in-time" approach. In previous years, some mills maintained stocks of 5,000 to 13,000 tons, enough for 3-4 days of production. With finished product prices also falling due to weak demand, steel mills are adopting more aggressive strategies, such as selling at low prices to reduce inventory. This has led to increased competition and further downward pressure on prices.

Another factor is the tightness in capital availability. Both steel mills and major buyers are struggling with cash flow issues, making it difficult for smaller merchants to secure financing. This lack of liquidity is limiting buying activity and contributing to the overall bearish sentiment in the market.

Psychologically, many players are still recovering from losses experienced during the same period last year. This has created a cautious mindset, where most are hesitant to buy in anticipation of further declines. As a result, even though the Spring Festival holiday may bring a slight increase in demand, the rebound is likely to be limited. The operating rates of downstream facilities remain low, and billet purchases are still sluggish.

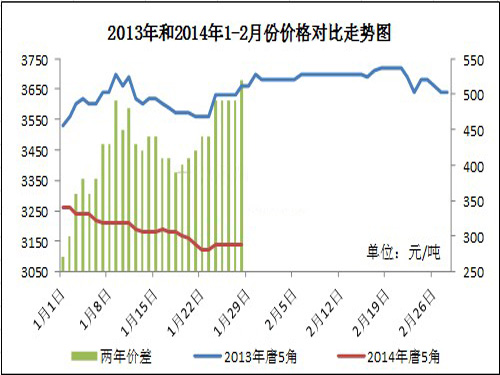

Tangshan billet prices are currently hovering between 2,830 and 2,870 yuan per ton, but the upward movement is minimal. For example, the price of Tangshan 5-angle steel fell from 3,260 yuan on January 1st to 3,140 yuan today, a drop of 120 yuan. In contrast, the same period last year saw an increase of 130 yuan. Similar trends are observed in other regions, such as Lancang, where Dongshan 10-14 slot steel dropped from 3,370 to 3,190 yuan, a decrease of 180 yuan. Wushao 5-angle steel also fell by 100 yuan to 3,270 yuan.

Despite the ongoing challenges, most large steel plants continue to operate during the Spring Festival, while smaller ones have either suspended production or are running at minimal capacity. According to Zhuochuang Information, factory inventories during the holiday could increase by 10,000–15,000 tons, while small factories maintain inventories at 7,000–16,000 tons, which is considered normal.

The main reasons for the lack of price recovery include weak downstream demand and continued financial constraints. Banks are still maintaining strict controls over the steel sector, and there is a possibility that merchants may resort to low-cost sales to free up capital. These factors are keeping the market under pressure.

In summary, the post-holiday market is still in a fragile state, with no clear signs of a strong recovery. However, some analysts expect a gradual upward trend to emerge by late February or early March, with an initial range of 50–100 yuan. As downstream industries begin to ramp up operations, demand and prices may slowly improve. Nevertheless, both steel mills and traders are closely watching the market, hoping for a long-term rebound.

As the saying goes, "After a long decline, a rise is inevitable." But for now, the market remains uncertain. While the "Jin San Yin Si" (the third and fourth months of the lunar calendar) traditionally bring some price increases, experts advise caution before the 15th day of the lunar month. Merchants are advised to remain patient and keep an eye on macroeconomic policies as they may influence future market movements.

Since the start of January, the section steel market has been on a downward spiral, with prices continuously dropping and showing no sign of recovery. Many traders are now questioning whether this slump will eventually reverse or if it's just the beginning of a longer decline. The market is in a state of uncertainty, and the outlook remains bleak for many players in the steel industry.

The raw material billet market has also struggled to find stability after a prolonged period of weakness. Steel billet prices began to fall in mid-December, and although there was hope for a rebound in January, the market continued to disappoint. From 3,040 yuan per ton on December 30 to 2,820 yuan today, that’s a total drop of 220 yuan. In January alone, the decline reached 160 yuan, indicating a sharper fall than expected. Compared to 3,280 yuan per ton in the same period last year, the current situation looks even more challenging. This sharp drop has raised concerns among market participants, especially as inventory levels remain high.

As of January 23, the mainstream stockpiles of Tangshan billets reached 666,000 tons, with 187,000 tons added in January. This is significantly lower than the 431-104 million tons recorded in January 2013, which saw 610,000 tons added. Additionally, the operating rate of rolling lines in billet mills has dropped to around 20-30%, hitting a low point. These figures suggest that while supply is under control, demand is weak, leading to further price pressure.

One key reason behind the weak performance is the reduced purchasing behavior from downstream users. Many mills have cut their billet purchase volume from about 20 days to just 10 days, opting for a "just-in-time" approach. In previous years, some mills maintained stocks of 5,000 to 13,000 tons, enough for 3-4 days of production. With finished product prices also falling due to weak demand, steel mills are adopting more aggressive strategies, such as selling at low prices to reduce inventory. This has led to increased competition and further downward pressure on prices.

Another factor is the tightness in capital availability. Both steel mills and major buyers are struggling with cash flow issues, making it difficult for smaller merchants to secure financing. This lack of liquidity is limiting buying activity and contributing to the overall bearish sentiment in the market.

Psychologically, many players are still recovering from losses experienced during the same period last year. This has created a cautious mindset, where most are hesitant to buy in anticipation of further declines. As a result, even though the Spring Festival holiday may bring a slight increase in demand, the rebound is likely to be limited. The operating rates of downstream facilities remain low, and billet purchases are still sluggish.

Tangshan billet prices are currently hovering between 2,830 and 2,870 yuan per ton, but the upward movement is minimal. For example, the price of Tangshan 5-angle steel fell from 3,260 yuan on January 1st to 3,140 yuan today, a drop of 120 yuan. In contrast, the same period last year saw an increase of 130 yuan. Similar trends are observed in other regions, such as Lancang, where Dongshan 10-14 slot steel dropped from 3,370 to 3,190 yuan, a decrease of 180 yuan. Wushao 5-angle steel also fell by 100 yuan to 3,270 yuan.

Despite the ongoing challenges, most large steel plants continue to operate during the Spring Festival, while smaller ones have either suspended production or are running at minimal capacity. According to Zhuochuang Information, factory inventories during the holiday could increase by 10,000–15,000 tons, while small factories maintain inventories at 7,000–16,000 tons, which is considered normal.

The main reasons for the lack of price recovery include weak downstream demand and continued financial constraints. Banks are still maintaining strict controls over the steel sector, and there is a possibility that merchants may resort to low-cost sales to free up capital. These factors are keeping the market under pressure.

In summary, the post-holiday market is still in a fragile state, with no clear signs of a strong recovery. However, some analysts expect a gradual upward trend to emerge by late February or early March, with an initial range of 50–100 yuan. As downstream industries begin to ramp up operations, demand and prices may slowly improve. Nevertheless, both steel mills and traders are closely watching the market, hoping for a long-term rebound.

As the saying goes, "After a long decline, a rise is inevitable." But for now, the market remains uncertain. While the "Jin San Yin Si" (the third and fourth months of the lunar calendar) traditionally bring some price increases, experts advise caution before the 15th day of the lunar month. Merchants are advised to remain patient and keep an eye on macroeconomic policies as they may influence future market movements.Dies And Hand Tools,Grommet Kit,Grommet Punch,Eyelet Punch Tool

NINGBO ZONGLAN MECHANICAL AND ELECTRICAL EQUIPMENT MANUFACTURE CO., LTD , https://www.zonglaneyelet.com